Artificial Intelligence and the Arithmetic of Capital

Ram Ahluwalia on AI, liquidity, and capital discipline

Artificial intelligence inspires awe for good reason. Software now writes code, agents draft contracts, models compress months of research into minutes, and the direction of travel is unmistakable. The productivity gains are visible in real time, and few serious observers doubt that AI will alter the structure of companies and the daily work of knowledge employees.

Ram Ahluwalia, Founder and CEO of Lumida Wealth, does not dispute any of that. His focus is elsewhere. In our conversation, he returned repeatedly to a quieter constraint: artificial intelligence has a capital markets dependency. The largest models require vast compute commitments, and those commitments are not metaphors. They are long term contracts with data centers, hyperscalers, and counterparties who expect to be paid. Innovation, in this case, sits atop an enormous stack of financial obligations.

OpenAI, by its own disclosures, carries committed obligations that approach a trillion dollars while generating revenue that remains a fraction of that figure. Even generous assumptions about growth do not easily reconcile the scale of the commitments with the income currently produced. These obligations extend over years, but time does not dissolve arithmetic. More than one company in this ecosystem would have to reach extraordinary revenue levels for the full structure to justify itself, and the capital required to bridge that distance must be supplied by investors who remain willing to fund it.

The technology may prove extraordinary. The math still governs.

Clip from the interview: The capital obligations behind today’s AI valuations.

That observation does not amount to a forecast of failure. It is instead a recognition of dependency. The expansion of AI depends on the continued cooperation of capital markets, on equity investors prepared to underwrite dilution, on debt investors comfortable with duration, and on sovereign pools of capital willing to absorb risk. When liquidity is abundant, those channels remain open. When it tightens, expansion slows regardless of technical progress.

The exposure is not confined to start ups. Major public companies hold revenue performance obligations tied to these contracts, which means that AI risk is distributed across balance sheets that sit inside the S&P 500. The story is not contained within a single private valuation; it is embedded within large public enterprises whose share prices reflect those commitments.

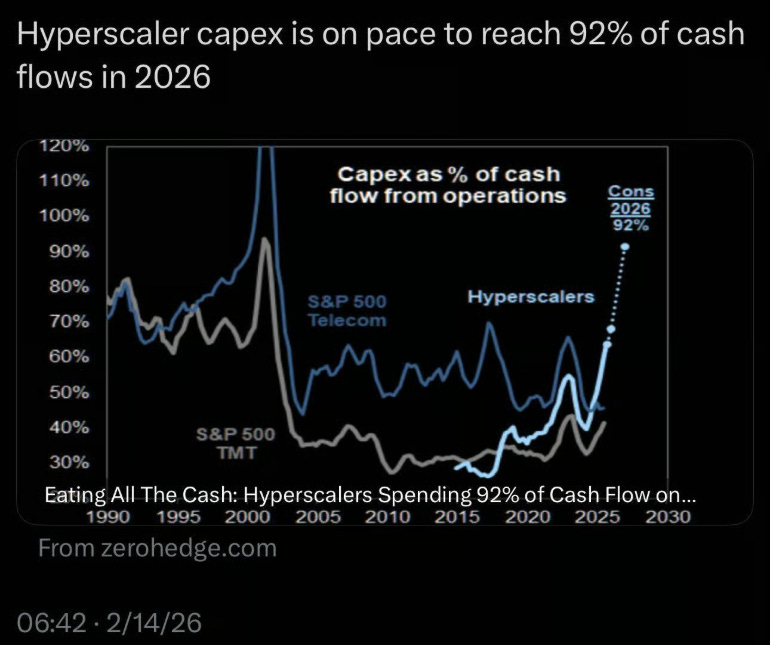

How much does hyperscaler capex depend on real revenues from AI companies like OpenAI?

This helps explain the rotation now visible in markets. Technology leadership has softened while energy, industrials, and value oriented companies have found relative strength. Ram described the shift as moving from zeros and ones to the physical economy, a phrase that captures a reweighting of capital toward businesses with tangible output and durable cash flow. There is no hostility toward innovation in that shift. It reflects a reassessment of where earnings are presently certain and where they remain projected.

Arithmetic reality in a simple picture.

The conversation moved, at one point, to venture capital and the direction of funding over the last cycle. Capital flowed enthusiastically toward tokens, agentic abstractions, and thematic constructs that promised participation in the future, while small businesses that continue to generate employment and free cash flow received far less attention. The spectacle of exponential innovation commanded headlines. The steady compounding of profitable enterprises did not.

Capital allocation, however, eventually returns to earnings power. When valuation drifts too far from cash flow, it corrects not out of moral judgment but because balance sheets impose discipline.

Bitcoin offered a revealing moment in this regard. At a conference filled with conviction, Ram described telling a large holder that Bitcoin should be managed rather than revered. In his view, it is an asset class that moves through cycles, experiences overextension and retrenchment, and belongs inside a portfolio governed by risk management rather than ideology. That posture does not diminish the asset. It situates it within the same framework applied to software, energy, or industrial stocks.

What ran through the entire discussion was not doubt about technological progress but respect for capital structure. Artificial intelligence may transform productivity and reshape competitive advantage, yet it remains funded by contracts that must be honored and investors who must be persuaded. Innovation attracts capital quickly. Sustained prosperity requires that capital be stewarded with discipline.

The future may well be defined by machines that think alongside us. The path they take will be shaped less by their brilliance than by the arithmetic that finances their rise.

Read Ram’s report on his Lumida Insights page HERE:

Full interview.

Thank you very much to our sponsors:

Truflation: BUY Truflation products/services and save 10% using code BOBDEW10. Learn about what prices are actually doing by going to https://truflation.com/marketplace/us-inflation-rate

Foundation: Protect your Bitcoin using the latest off-line technology with easy-to-use Passport. Their next product, Passport Prime will protect all passwords off-line with even-better technology. https://foundation.xyz/

River Financial: If not cold storage for your Bitcoin, I’d highly recommend River for buying and holding- River is engineered to protect your Bitcoin over the long run. Use this link for discounts: https://river.com/signup?r=T7GGAF7G

very interesting article, Bob, thank you. It’s so remarkable that you and I and everyone gets these powerful tools for free, in gemini or grok or wherever, you can type in complicated questions and get immediate thoughtful answers, even if not perfect. But to your point, someone’s got to pay for the enormous energy burn that goes into these calculations. consumers are not going to pay much if anything for AI-powered websearch. advertisers will have to pay for that. which implies continued disruption to traditional forms of marketing as we’re already seeing. the more interesting question is whether companies are getting AI tools from providers for less than full cost, and what are the true ROIs. we can all see that LLMs have enormous power, but as people point out there is a “jagged edge” to AI capabilities, meaning that the reliability and accuracy isn’t there for many applications with low tolerance for risk. the shakeout you are referencing is probably only getting started — but that’s a wild guess from someone who doesn’t know